Responding to Moody’s Investors Services’ recent assessment that the territory will likely be forced to restructure its debt, Gov. Albert Bryan Jr. said in a statement issued this week by Government House that the territory should “take another serious look” at trying to refinance some of its bond debt.

At the end of March, Moody’s issued a review saying the USVI’s extremely poor Caa3 and Caa2 ratings reflect: a small and highly concentrated economy, government finances that have been severely strained, a very poorly funded pension system that is rapidly depleting its asset base, financial reporting and other governance challenges and the government’s loss of capital markets access since 2017.

That last item is a reference to the fact that lenders have been unwilling to enter into municipal bond lending arrangements with the territory since a failed bond bid in 2017. (See V.I. Bond Sale Delayed As Investors Request More Time)

“Despite some recent improvement in the government’s liquidity and near-term financial position, the rating incorporates the risk that the reemergence of a significant structural deficit, combined with the expected insolvency of the Government Employees’ Retirement System, will lead the government to restructure its debt,” Moody’s concludes in its March 29 release.

Bryan has proposed creating a new entity to take control of federal alcohol excise taxes as a way of reassuring lenders the territory will be unable to divert any funding to other priorities. His administration hopes this move will entice lenders to refinance the territory’s $2 billion debt at lower interest rates, saving tens of millions of dollars per year.

The Legislature voted down the plan on Dec. 8, prompting Bryan to renew the push and call a special session at the end of the year to consider it again. At that session, the Legislature voted to send the measure to committee for more in-depth review.

In Bryan’s recent response, he pointed to a recent Third Circuit court decision that the government is not liable for some $43 million in interest, suggesting it is good news.

“This is not a loss for the GERS or the V.I. by any means. It underscores the urgency with which the executive and legislative branches need to work together to address and put forward a comprehensive solution to this problem,” Bryan said. “In the judgment, the court clearly defines that it is the duty of the Legislature to address the funding needed, and by working collectively, I believe we can solve this issue on behalf of the people of the Virgin Islands.”

“As evidence of our commitment, the Government of the Virgin Islands has paid millions to GERS over the years, none of which they applied to the balance they claim is due. It is time to take another serious look at refinancing our bond debt to achieve lower rates, which will allow us to put more money into the system,” Bryan said in his statement.

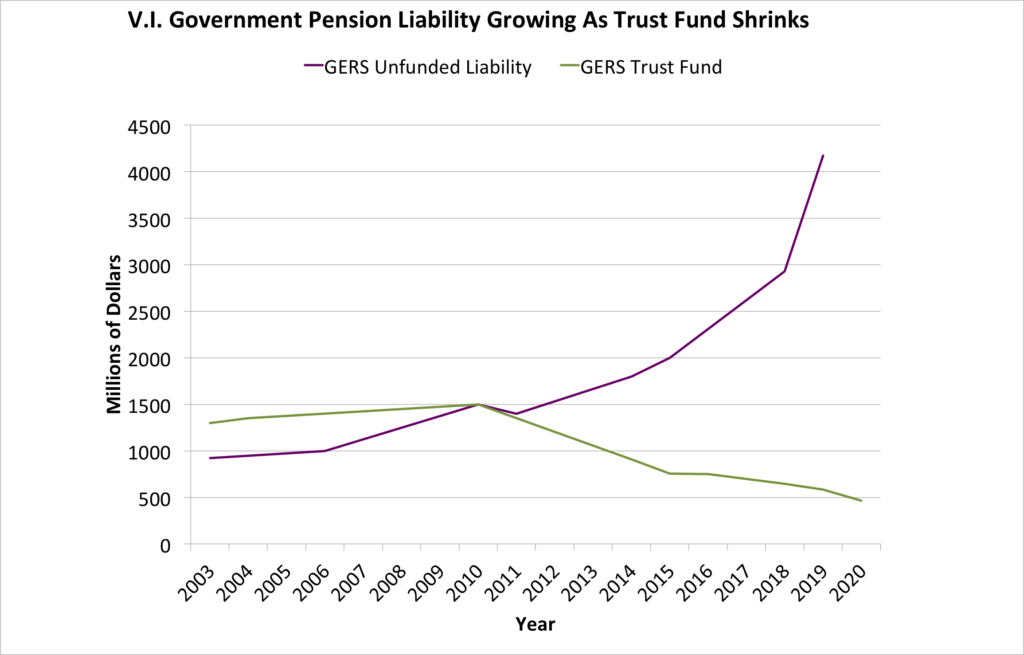

The statement from Government House acknowledged that the projected failure of GERS by 2024 may force the territory to restructure.

The Moody’s assessment said that regardless of whether the GVI paid the amount overturned by the Third Circuit, the retirement system is likely to fail in 2024.

“We estimate that GERS would have to cut benefit outflows to retirees by around 50 percent once its assets are depleted if its only sources of income are the USVI’s statutory contributions and active member contributions,” Moody’s reported, which Government House quoted in its statement.

“A benefit cut of any significant magnitude is unlikely to occur, in our view, without a broader restructuring of the USVI’s other debts and obligations to bondholders,” the Moody’s report said and Government House repeated.

Government House ended its statement by saying the “Bryan-Roach administration is committed to transparency, stabilizing the economy, restoring trust in the government and ensuring the disaster recovery is completed as quickly as possible.”

See the Source’s series here to learn more about the territory’s fiscal crisis.

{kind=link}